State of Venture Capital in Crypto, Q1 2025

Key Takeaways:

-

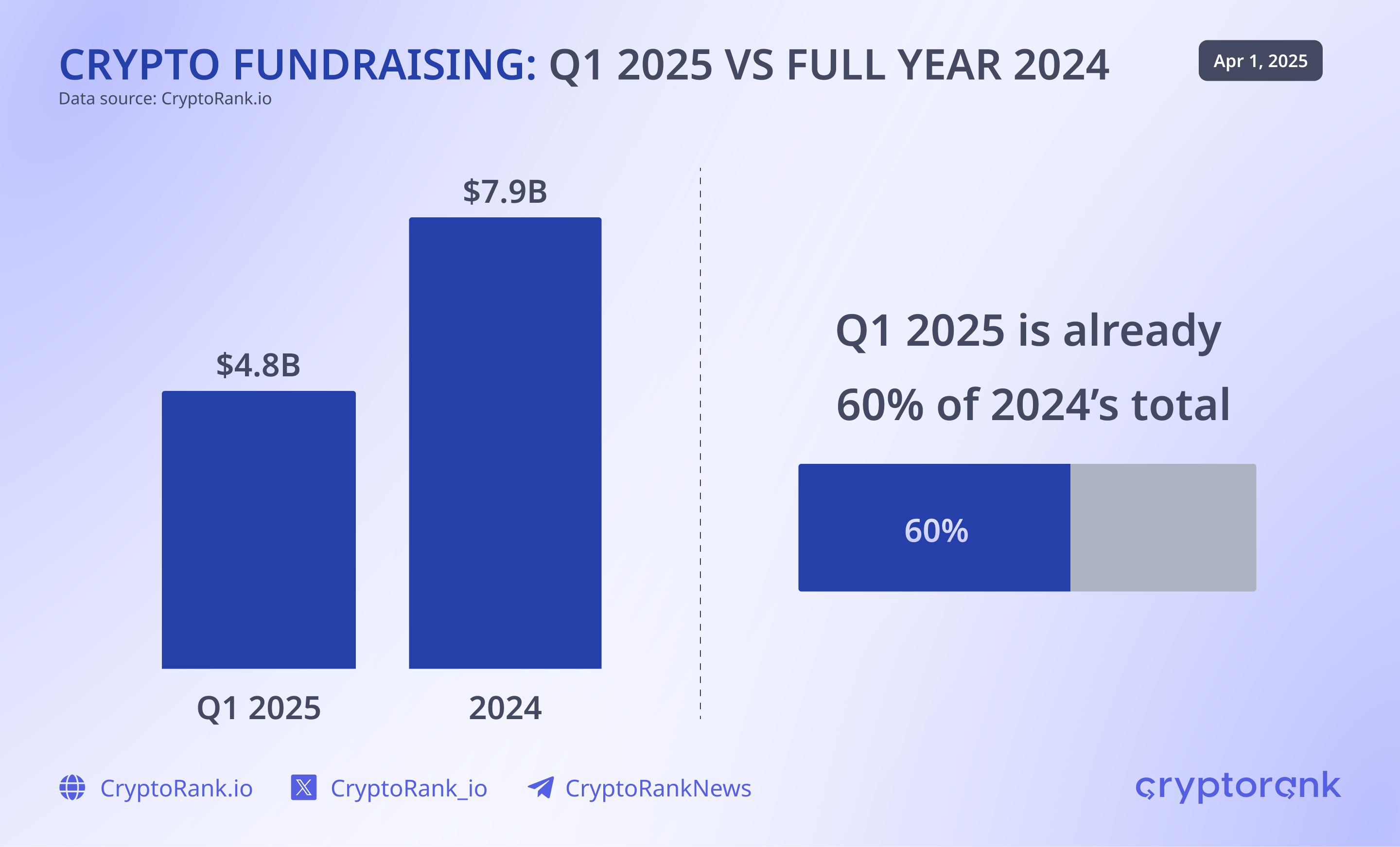

Crypto VC funding reached $4.8 billion in Q1 2025, the highest since Q3 2022.

-

The $2 billion Binance deal became the largest single investment in crypto VC history.

-

Q1 2025 funding equaled 60% of total VC capital deployed in all of 2024.

-

US-based investors participated in nearly 215 deals, maintaining the country’s leading role.

The first quarter of 2025 began with momentum, but early optimism quickly gave way to renewed caution. Bitcoin closed the quarter down 11%, which reversed part of its early gains as macroeconomic uncertainty and fading risk appetite weighed on markets. While volatility remains elevated, the current cycle marks a departure from prior retail-driven booms, as institutional presence and regulatory engagement continue to grow.

At the global level, the macro environment remains fragile. The IMF projects global growth at 3.3% for 2025 and 2026, well below the historical average of 3.7%, while the World Bank expects an even slower 2.7%. Trade tensions have escalated following a new round of US tariffs. The result has been a rise in retaliatory actions and protectionism, which further disrupted global trade flows and darkening an already muted growth outlook.

Amid this, crypto markets are entering a distinct new phase. Structural shifts, including greater regulatory clarity and deepening institutional participation, are fueling fresh momentum in venture fundraising. Early signals point to strength across a number of emerging sectors, even as broader market sentiment remains cautious. While short-term headwinds persist, the foundations are being laid for long-term capital formation and sector-wide maturation.

State of the Fundraising

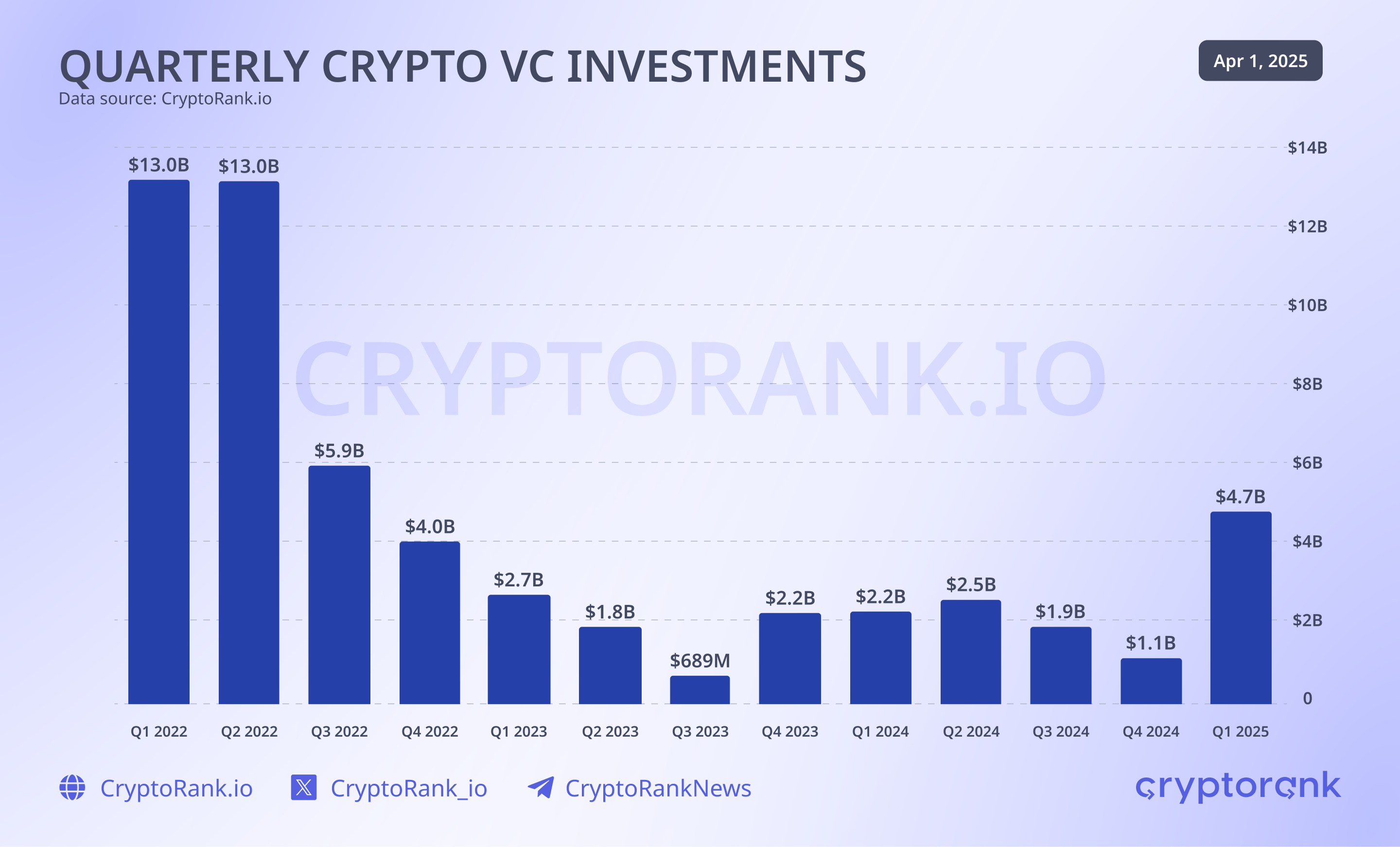

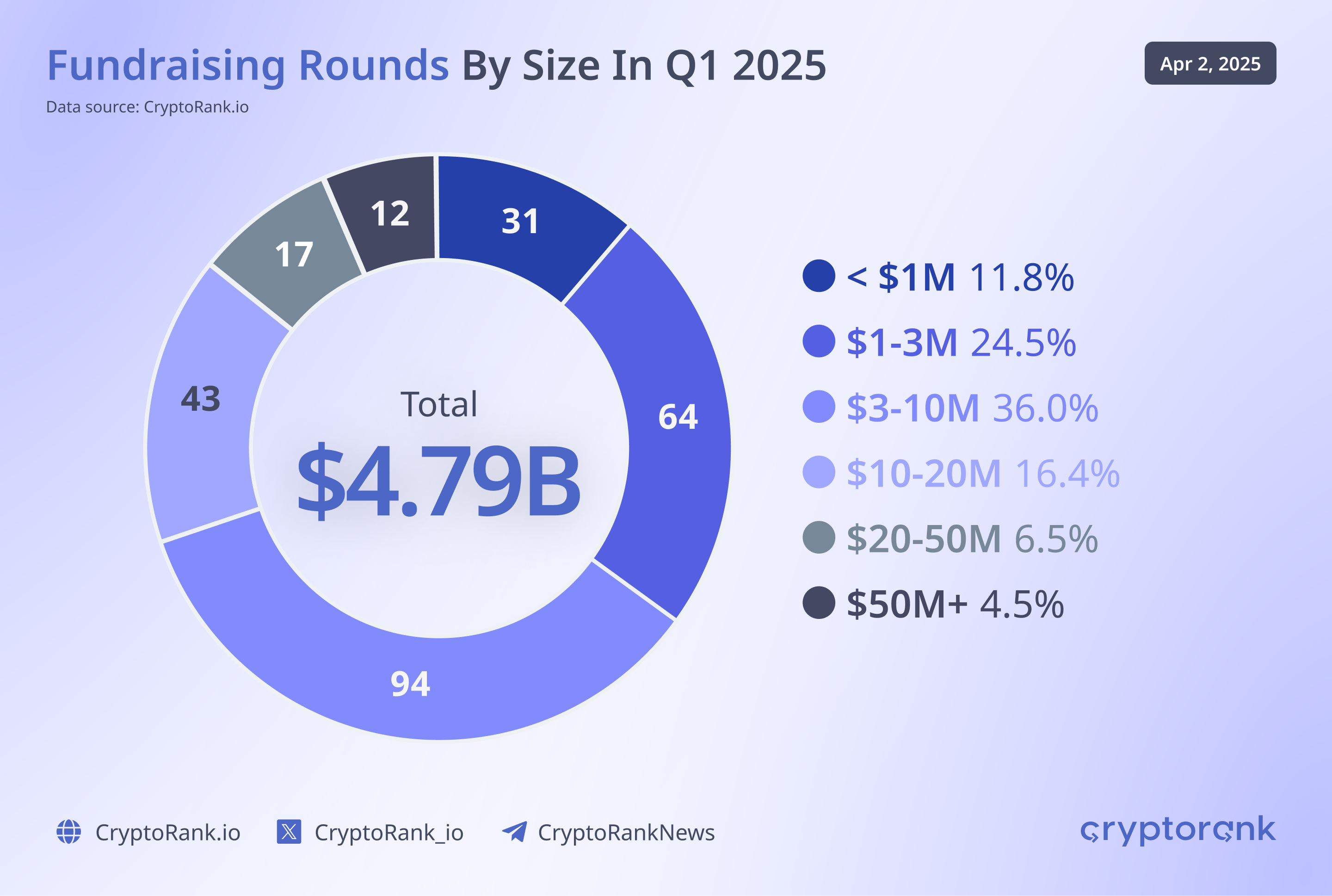

Despite the fragile macro backdrop, venture capital inflows into crypto surged in Q1 2025 and reached $4.8 billion. This marked the strongest quarter for crypto VC since Q3 2022. A major contributor was the $2 billion investment into Binance by Abu Dhabi-based MGX, now the largest single deal in crypto VC history. The scale of this raise highlights a renewed institutional appetite for late-stage infrastructure plays, even as broader markets remain cautious.

However, while the total capital invested increased, the number of rounds closed in Q1 saw a slight decline. By this measure, the market is in a healthier position than it was in 2023, although both Q1 and Q2 of 2024 showed higher number of investment deals overall.

Still, the current quarter offers reasons for optimism. Venture capital allocations in Q1 2025 already account for 60 percent of the total capital deployed during all of 2024. This acceleration suggests growing conviction among investors that crypto may be entering a new phase of adoption, with capital inflows potentially signaling the early stages of market revival.

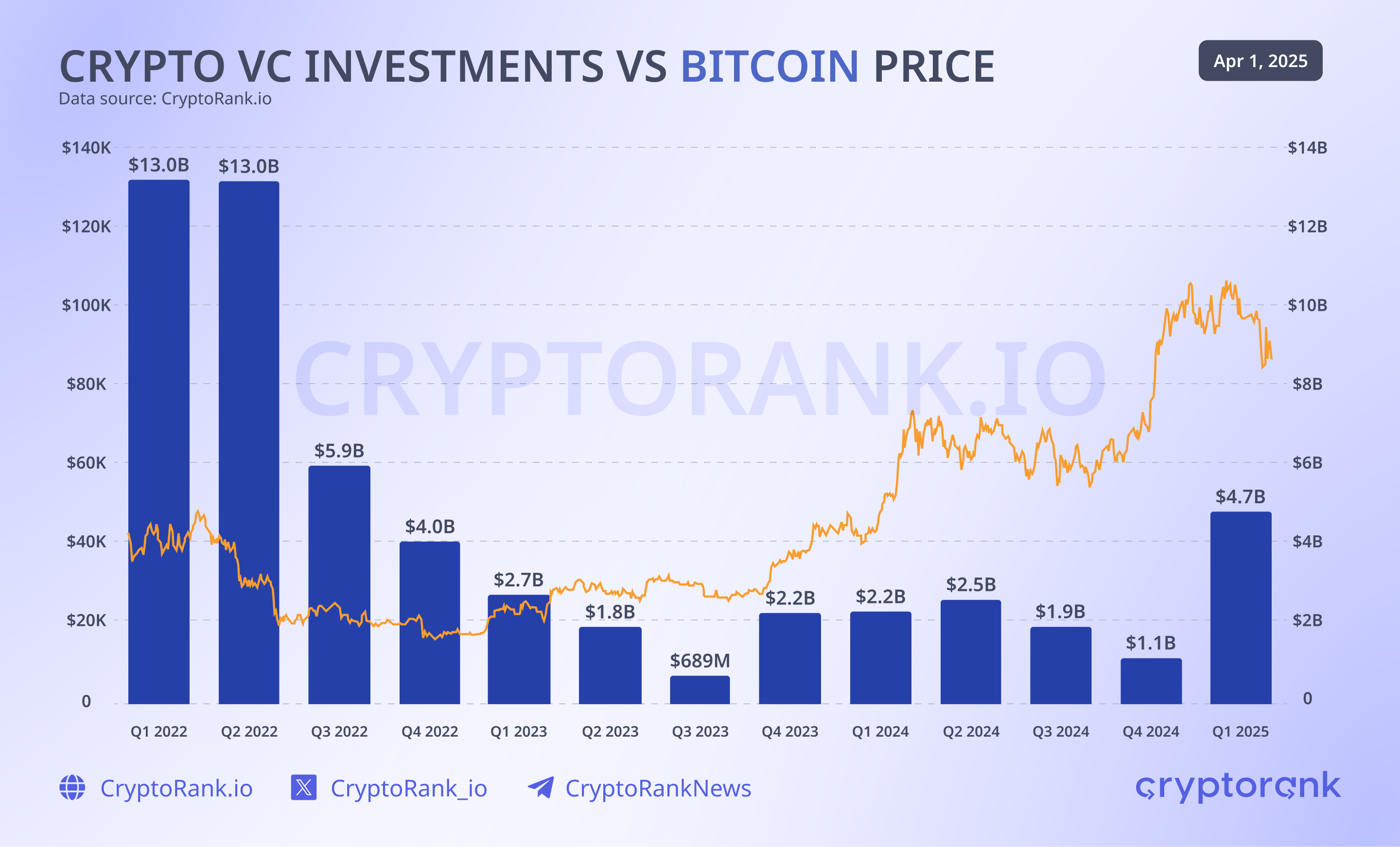

Compared to previous cycles, the correlation between Bitcoin price action and venture capital activity has become less immediate. VC investments now appear to lag one to two quarters behind major price movements. Strong BTC performance in Q3 and Q4 of last year translated into increased funding for crypto startups in Q1 2025. However, this dynamic also suggests that the recent price softness may lead to a slowdown in venture activity in the coming quarters.

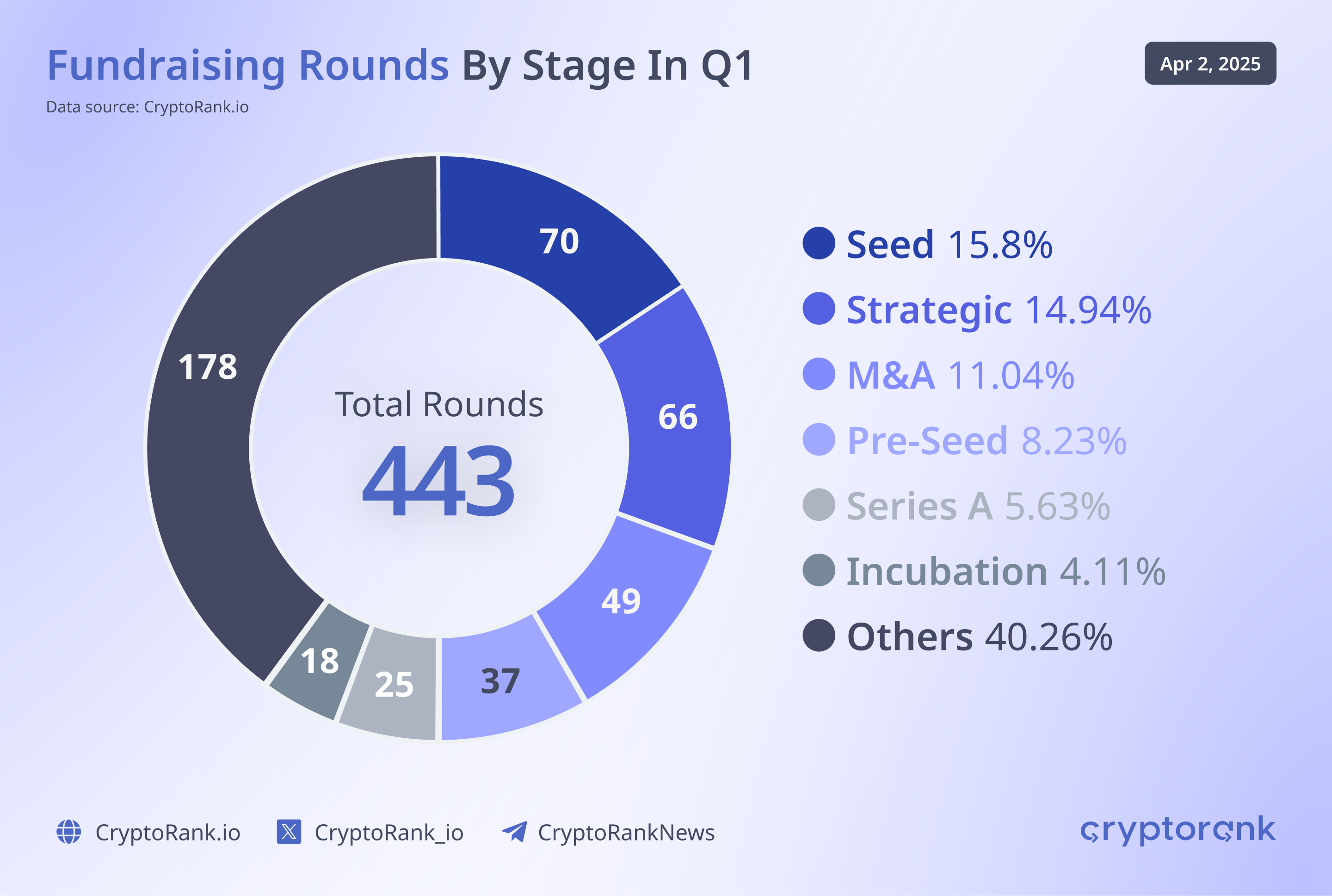

As usual, Seed rounds accounted for the majority of deals in Q1. This trend reinforces the view that the crypto startup ecosystem remains in its early stages, even as the broader blockchain industry approaches its second decade of development. The concentration of early-stage funding highlights both the nascency of new verticals and the ongoing search for scalable, investable business models in the space.

Notably, several high-profile mergers and acquisitions took place in Q1 2025, which signals a growing interest in consolidation among large crypto firms. Kraken acquired futures trading platform NinjaTrader for $1.5 billion, while MoonPay completed a $175 million acquisition of Helio. The rise in M&A activity reflects a maturing market, where established players are actively looking to expand through strategic acquisitions rather than organic growth.

On the valuation side, the median valuation of crypto startups saw a slight decline, returning to levels last seen in mid-2024. This suggests the industry remains far below the peaks of 2022 and early 2023, a period when blockchain startups attracted investor interest despite a broader market downturn. Similarly, the altcoin market showed signs of weakness, even amid strong BTC performance and renewed enthusiasm for memecoins. Venture capital appears to be shifting focus toward other sectors, with artificial intelligence seems a leading area of interest.

Smaller fundraising rounds under $10 million still accounted for nearly two-thirds of total deal count in Q1, but the presence of larger raises is becoming more noticeable. Twelve large-scale deals (over $50 million in size) closed during the quarter, signaling that mature, high-impact projects are gaining traction with investors. This trend points to a broadening of the market, where both early-stage experimentation and later-stage scaling coexist, and where capital is increasingly flowing to teams with proven execution or strong institutional support.

Driven by the $2 billion Binance deal, Malta took the lead in jurisdictional fundraising activity in Q1. However, The United States was the truly dominant jurisdiction, which continued to host the majority of venture-backed projects and capital. Meanwhile, new activity is steadily emerging across Asia, with Japan, China, and Hong Kong seeing increased project formation and growing investor interest. This geographic diversification highlights the global nature of crypto venture capital and the increase in competitiveness of non-Western markets.

Sectors Overview: What Caught Investors’ Eyes?

Venture capital in Q1 2025 concentrated around three core categories: centralized finance (CeFi), blockchain infrastructure, and blockchain services. These sectors continue to attract capital due to their clearer paths to revenue and user retention. Notable examples include Phantom, the Solana-native wallet, and Walrus, a DePIN protocol, both of which illustrate the market’s preference for products with strong traction and practical utility.

On the other hand, DeFi ranked among the top categories by number of closed funding rounds in Q1. While the total capital raised in the sector remained modest, investor interest in decentralized finance persists. The smaller deal sizes and lower valuations reflect the broader state of the crypto market and the current cooling of the DeFi narrative. Still, the high number of investment rounds suggests that investors continue to view the sector as a space for experimentation and long-term potential, even if near-term capital deployment remains conservative.

Investor continued to show appetite across key emerging segments. AI, DePIN, and real-world assets (RWA) stood out as some of the most attractive categories, which draw attention from both crypto-native and traditional venture firms. These sectors reflect a broader shift toward use cases with real-world integration, infrastructure potential, and crossover appeal beyond the crypto-native user base.

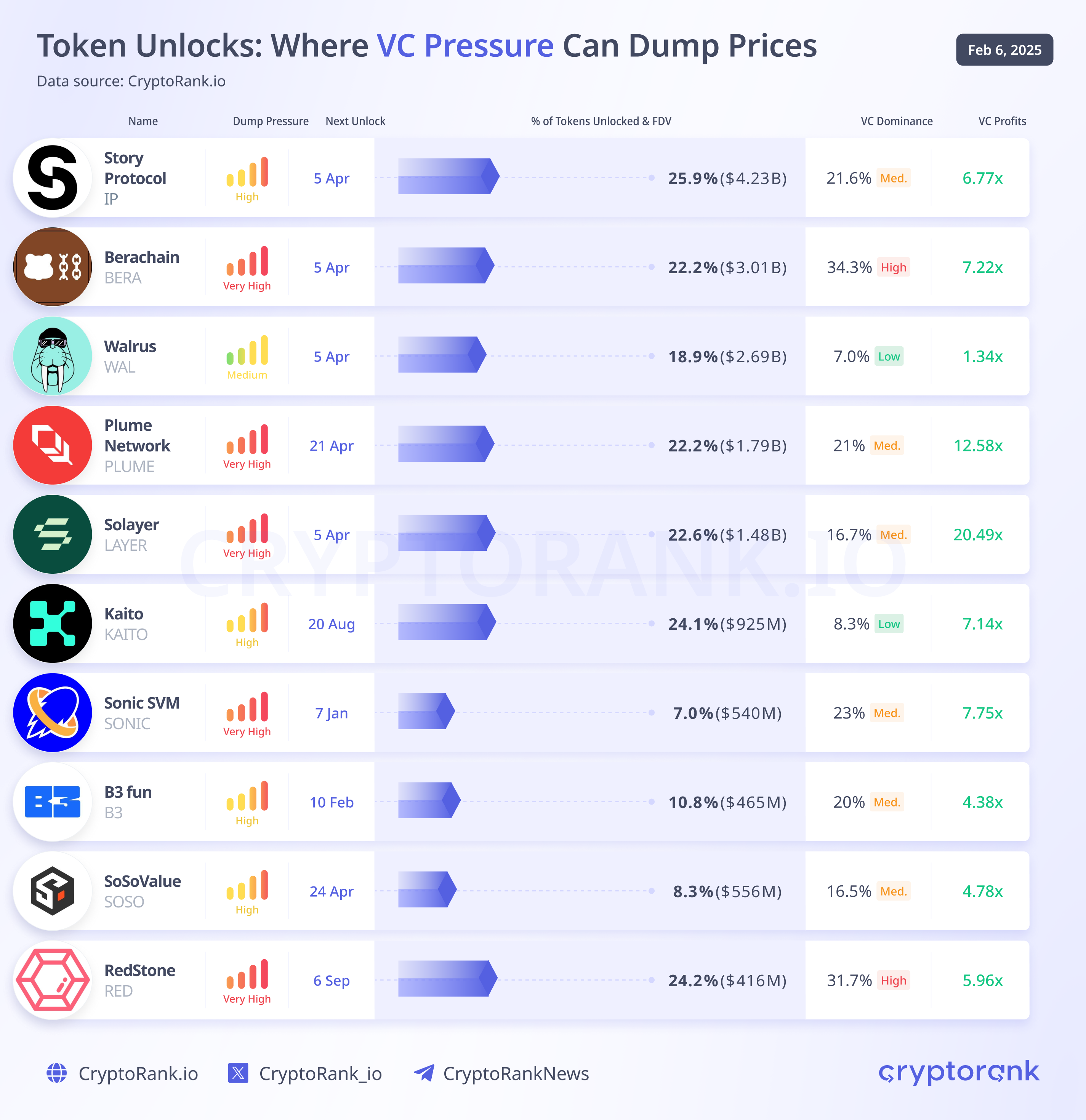

In Q1, several large-cap, VC-backed tokens entered the market, which brought nearly $20 billion in to-be-unlocked value. These launches mark a significant wave of token distribution that will shape market dynamics in the coming quarters. Retail investors should closely monitor unlock schedules for projects like Story Protocol, Berachain, and Plume Network, all of which have notably low float ratios. These structures can amplify price volatility and create asymmetric conditions between early investors and public market participants.

Highlights from Funds

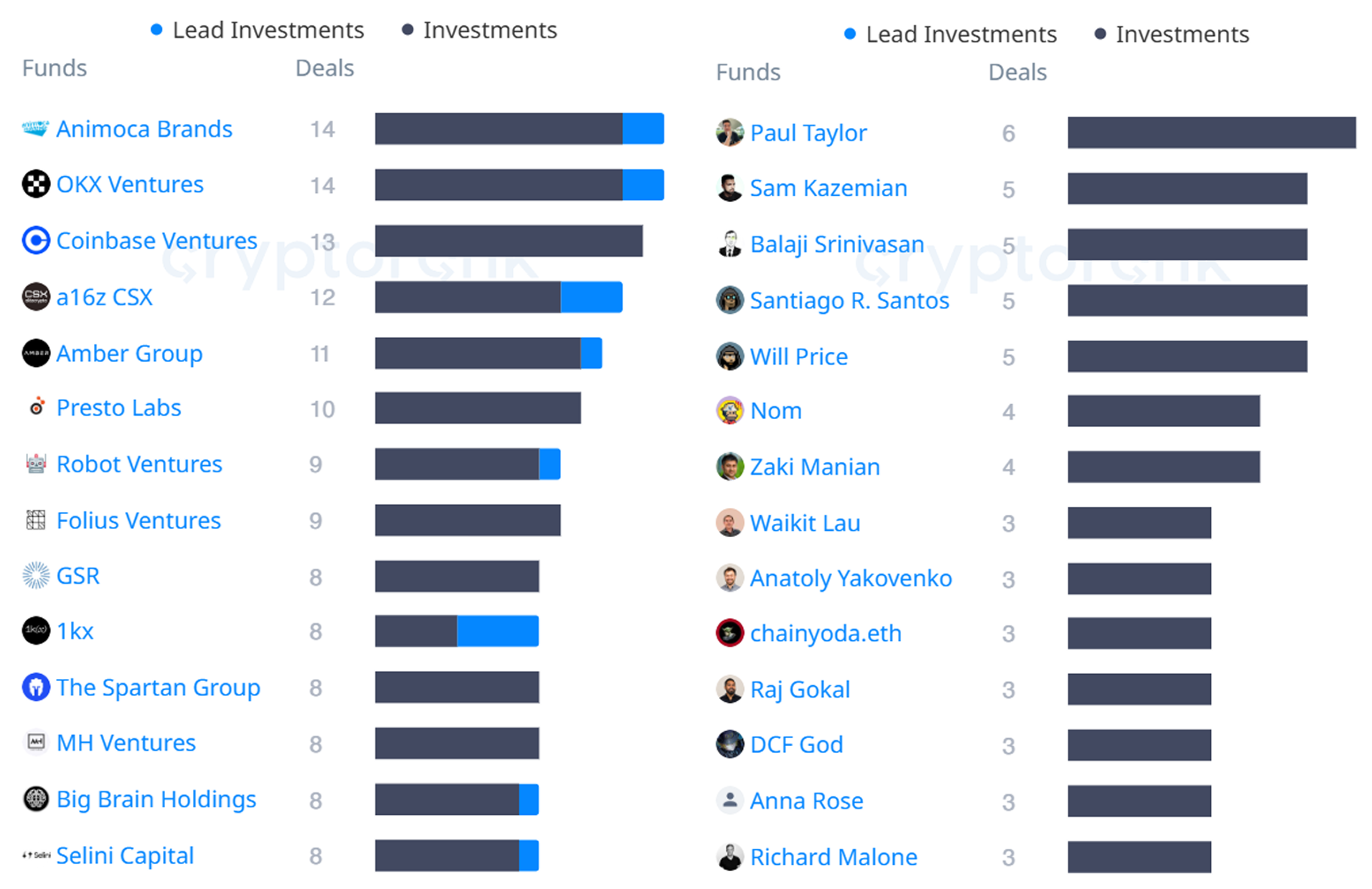

This quarter, Animoca Brands and OKX Ventures emerged as the most active crypto venture firms, with both focusing primarily on small- and mid-sized deals. Notably, among the top 15 most active VCs, only one other centralized exchange-backed fund appeared—Coinbase Ventures—highlighting a shift in influence away from CEX-affiliated capital toward more traditional VC investors.

The United States maintained its position as the leading hub for crypto venture activity, with US-based funds participating in nearly 215 funding rounds during Q1. Investors from Asia followed closely, with growing contributions from countries such as Japan and China, while select European nations also remained active. With a more relaxed regulatory tone and a pro-crypto shift in government posture, the US is well-positioned to strengthen its leadership. Backed by deep capital pools and an increasingly supportive policy environment, the country may solidify its role as the global center of crypto venture activity.

Closing Thoughts

Q1 2025 marked a clear rebound in crypto venture capital market, with $4.8 billion raised. This was the strongest quarterly total since Q3 2022. The $2 billion Binance deal played a central role, but the presence of twelve other large-scale (> $50M) rounds showed renewed institutional interest. With funding already reached 60% of 2024’s total capital deployed, investor appetite appears to be returning despite a slight decline in deal volume and ongoing macro uncertainty.

Capital flowed into sectors with proven utility and revenue potential, including CeFi, blockchain infrastructure, and services. New focus areas such as AI, DePIN, and real-world assets also drew strong interest. DeFi led in the number of rounds but saw smaller raise sizes, reflecting more conservative valuations. Nearly $20 billion in locked token value from recent launches is set to affect market conditions in the near term. The United States remained the dominant jurisdiction, supported by a favorable policy shift and deep venture capital presence. At the same time, Asia continued to expand its footprint, contributing to a more competitive and globally distributed investment landscape.

Disclaimer: This post was independently created by the author(s) for general informational purposes and does not necessarily reflect the views of ChainRank Analytics OÜ. The author(s) may hold cryptocurrencies mentioned in this report. This post is not investment advice. Conduct your own research and consult an independent financial, tax, or legal advisor before making any investment decisions. The information here does not constitute an offer or solicitation to buy or sell any financial instrument or participate in any trading strategy. Past performance is no guarantee of future results. Without the prior written consent of CryptoRank, no part of this report may be copied, photocopied, reproduced or redistributed in any form or by any means.